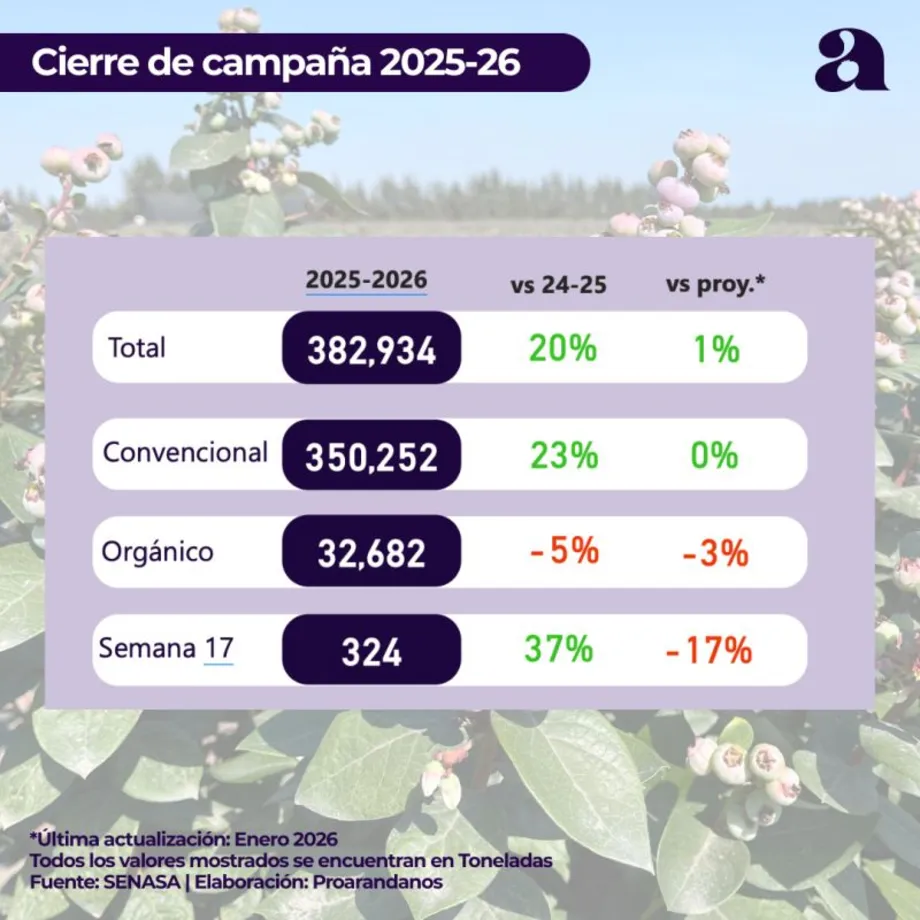

According to Proarándanos/SENASA data, the 2025-26 Peruvian blueberry season closes with a new increase in exports: total volumes reached 382,934 tonnes, with a strong recovery in conventional blueberries and weaker signals for organic production.

The 2025-26 season for Peruvian blueberries closes with final results that confirm Peru’s role as the world’s leading supplier in the category. According to data released by Proarándanos, total exports reached 382,934 tonnes, up 20% compared with the 2024-25 season and substantially in line with end-of-season projections, coming in 1% above estimates.

This figure is particularly significant because it follows a previous season affected by major production and climatic difficulties. The 2025-26 campaign therefore marks a phase of normalization and recovery, although not uniformly across segments, destinations and production areas. The main driver of growth was conventional blueberries, while the organic segment shows a more fragile trend.

Conventional blueberries recover strongly, organic declines

Conventional blueberries reached 350,252 tonnes, an increase of 23% compared with the previous season. This segment accounts for almost all the growth in Peruvian exports, confirming the country’s ability to quickly return to high availability levels after the production difficulties of the previous cycle.

The organic picture is more complex: volumes stood at 32,682 tonnes, down 5% compared with the 2024-25 season and 3% below projections. The figure points to an interesting divergence: while conventional blueberries are growing strongly again, organic production appears to be affected by greater commercial selectivity, production constraints or weaker demand momentum compared with the years of rapid expansion.

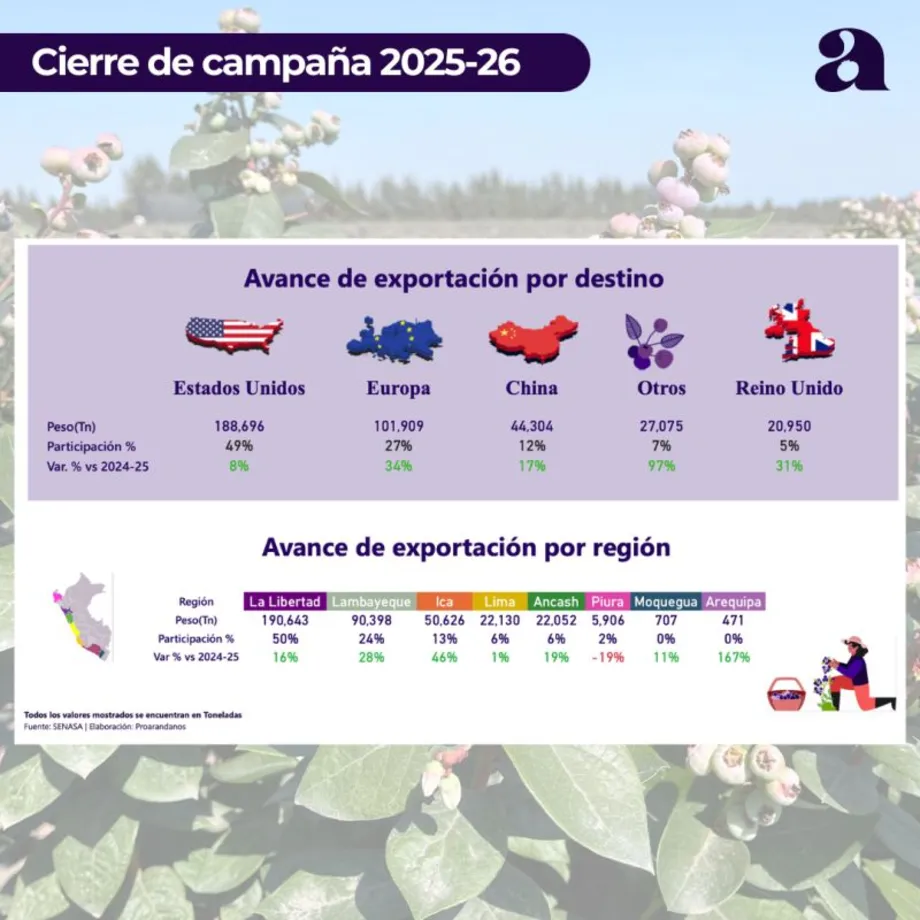

United States remains the leading market, but Europe grows faster

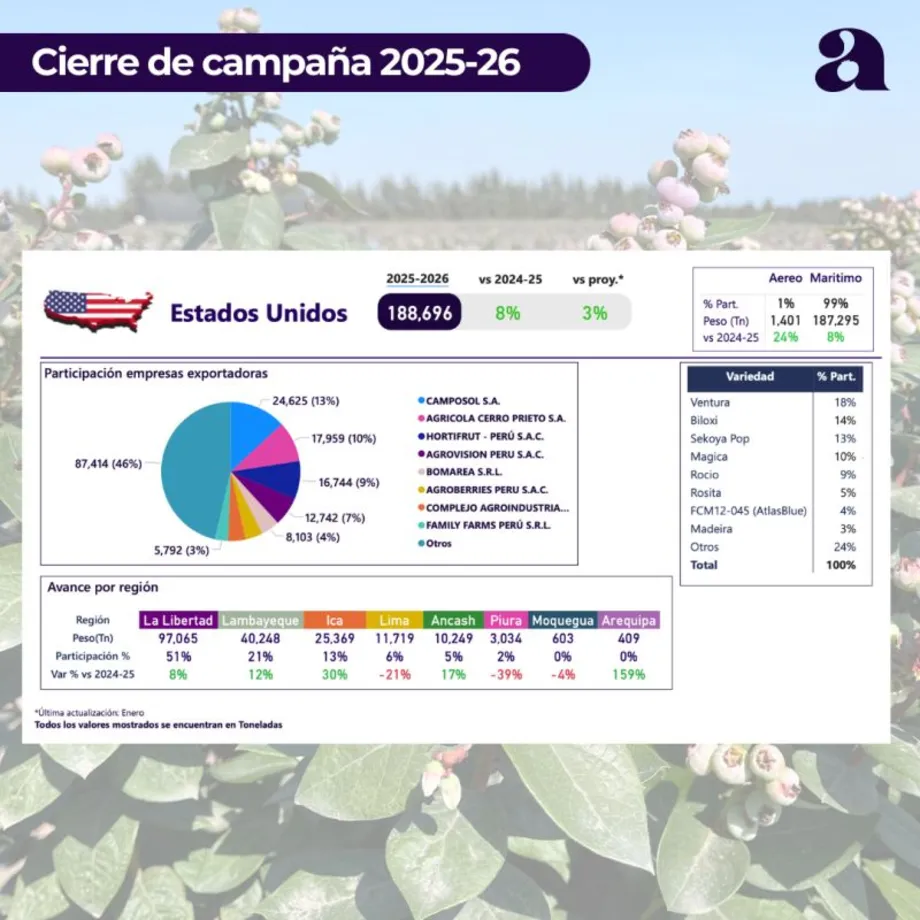

The United States remains by far the main destination for Peruvian blueberries. In the 2025-26 season, it absorbed 188,696 tonnes, equal to 49% of total exports, with growth of 8% compared with the previous season. The US market therefore confirms its central role, although its growth rate is lower than that of other destinations.

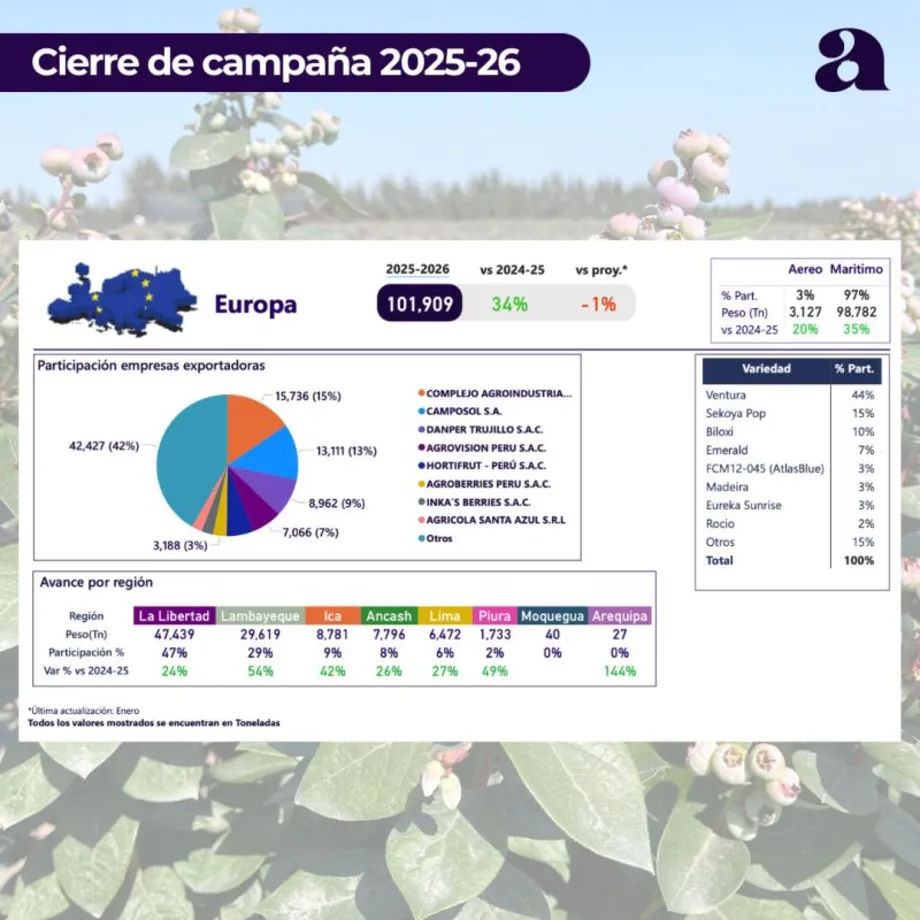

The most significant dynamic comes from Europe, which reached 101,909 tonnes, equal to 27% of Peruvian exports, with an increase of 34%. For the European berries system, this figure confirms Peru’s growing weight in the counter-season window and in supplying large-scale retail programmes, at a time when quality, size and continuity of supply are becoming increasingly decisive factors.

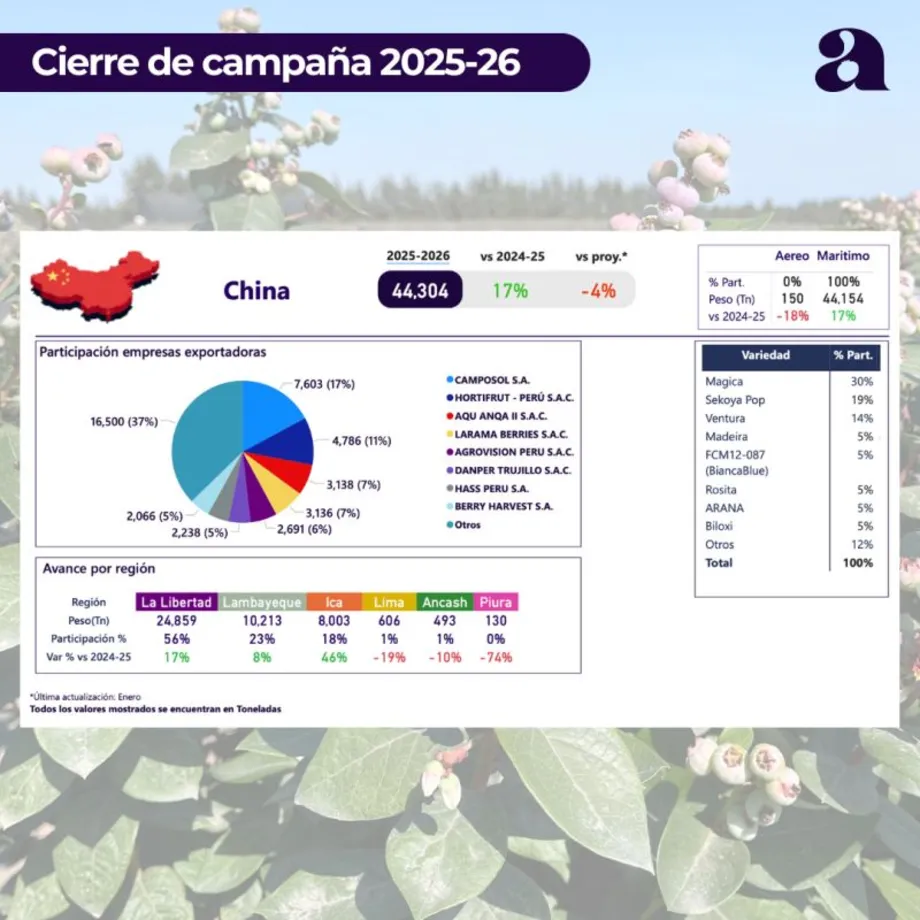

China ranks third with 44,304 tonnes, equal to 12% of the total and growth of 17%.

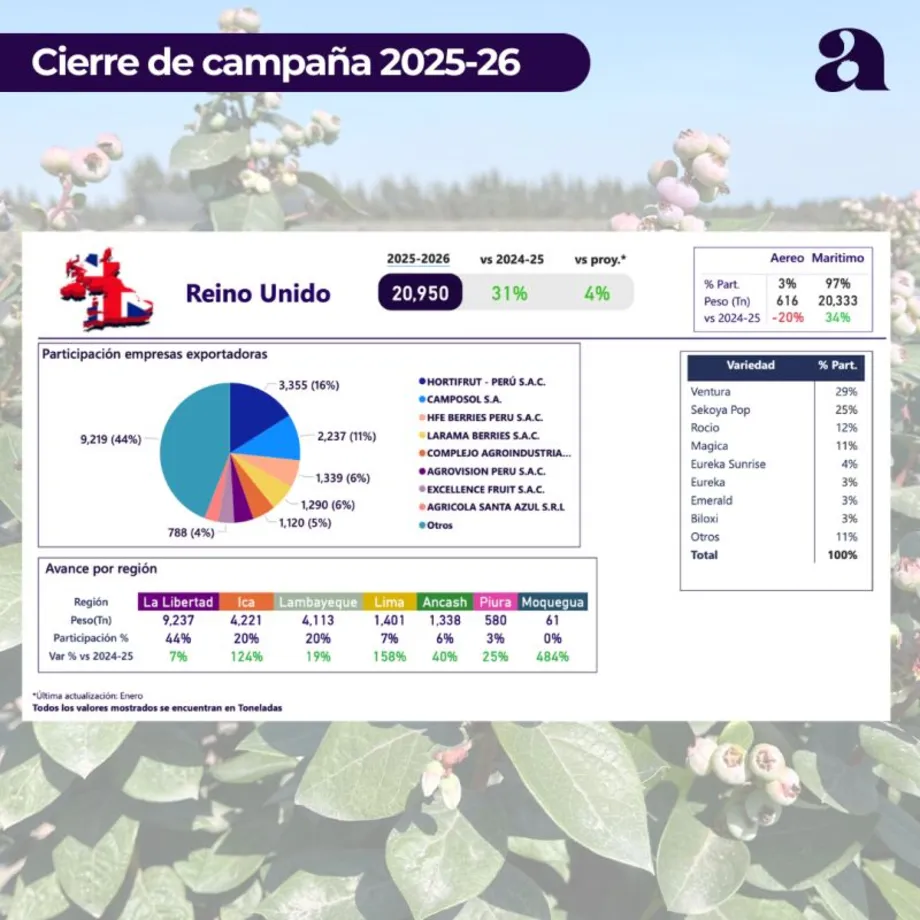

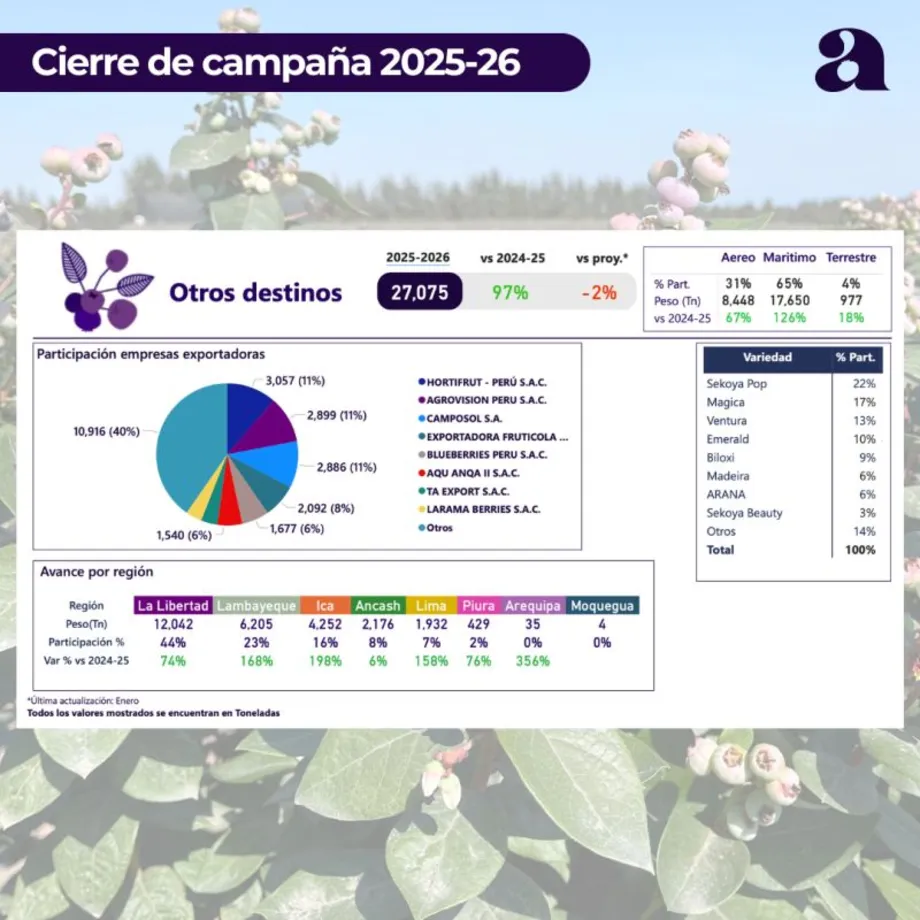

The United Kingdom reached 20,950 tonnes, up 31%, while other markets, grouped under “Other destinations”, reached 27,075 tonnes, with very strong growth of 97%. This last figure points to a gradual geographical diversification of Peruvian exports, even though the three main blocks — United States, Europe and China — continue to concentrate the dominant share of volumes.

La Libertad remains the productive heart of Peruvian blueberries

From a regional perspective, leadership remains firmly in the hands of La Libertad, which, with 190,643 tonnes, accounts for 50% of Peruvian exports. The region grew by 16% compared with the previous season and confirms its role as the country’s main production platform.

Second place goes to Lambayeque, with 90,398 tonnes and a 24% share, up 28%. It is followed by Ica, with 50,626 tonnes and an increase of 46%, Lima with 22,130 tonnes, Ancash with 22,052 tonnes and Piura with 5,906 tonnes, the latter down 19%. Moquegua and Arequipa remain marginal in terms of share, although they are also growing.

The regional reading confirms a still concentrated production structure, but with differentiated expansion dynamics. La Libertad remains the centre of gravity, while Lambayeque and Ica confirm themselves as key areas for future growth.

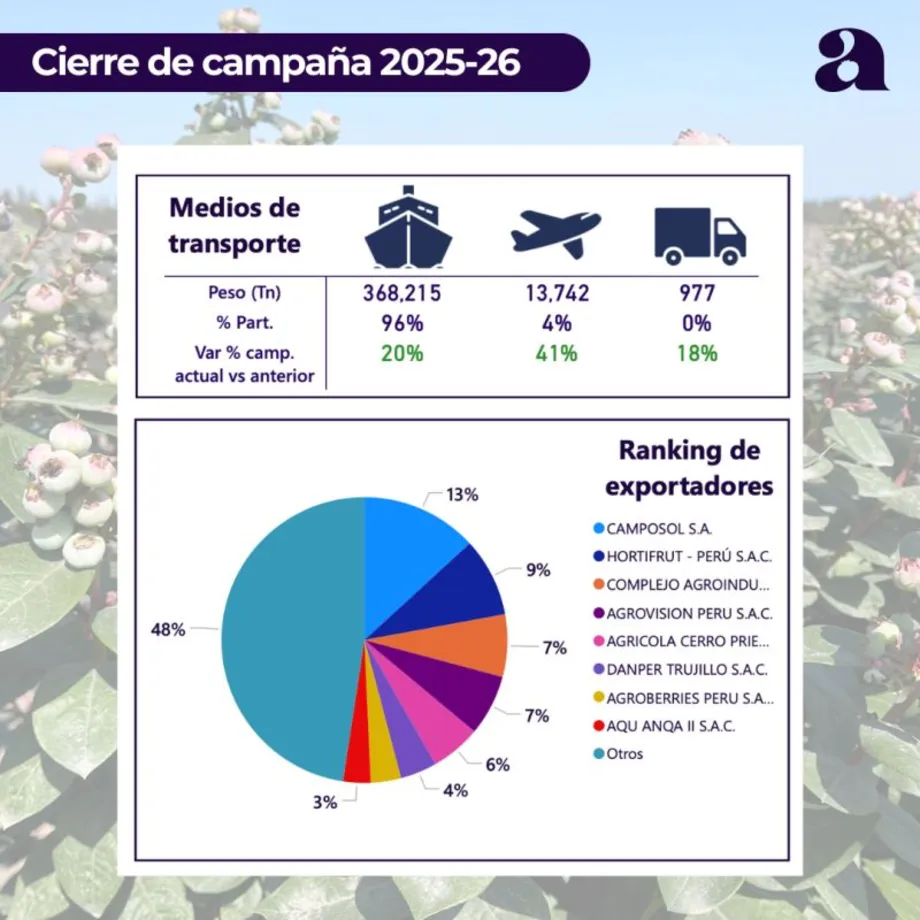

Logistics: 96% travels by sea

Peruvian blueberries remain a category strongly linked to maritime logistics. In the 2025-26 season, 368,215 tonnes were exported by sea, equal to 96% of the total, with growth of 20% compared with the previous season.

Air transport accounts for a much smaller share, at 4%, but with significant growth: 13,742 tonnes, up 41%. This figure may reflect specific needs linked to commercial windows, premium markets or the need for rapid response in phases of high demand. Land transport remains marginal, with 977 tonnes.

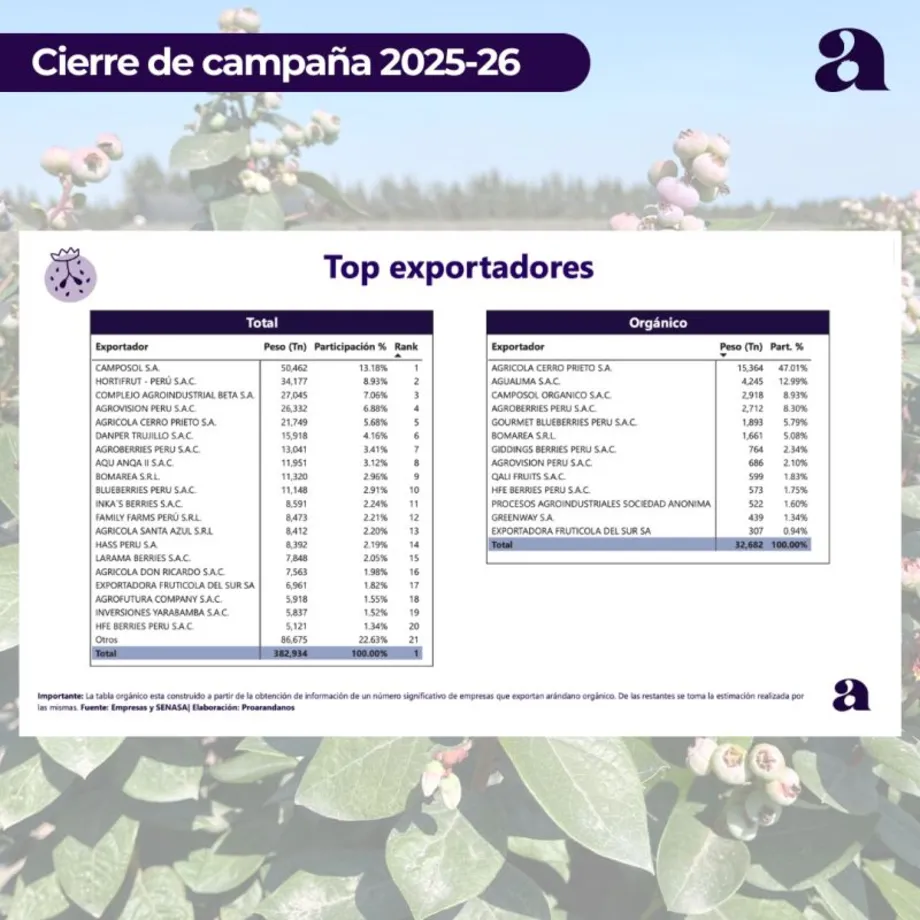

Camposol is the leading exporter, with strong concentration among the leaders

The exporter ranking confirms the weight of Peru’s large agro-industrial groups. Camposol S.A. closed in first place with 50,462 tonnes, equal to 13.18% of the total. It is followed by Hortifrut Perú S.A.C. with 34,177 tonnes, Complejo Agroindustrial Beta S.A. with 27,045 tonnes, Agrovision Peru S.A.C. with 26,332 tonnes and Agrícola Cerro Prieto S.A. with 21,749 tonnes.

Other leading operators include Danper Trujillo S.A.C., Agroberries Peru S.A.C., Aqu Anqa II S.A.C., Bomarea S.R.L. and Blueberries Peru S.A.C..

In the organic segment, however, concentration appears much higher: Agrícola Cerro Prieto is the leading exporter with 15,364 tonnes and a share of 47.01%, followed by Agualima S.A.C. and Camposol Orgánico S.A.C..

Five companies began exporting in 2025-26, achieving volumes between 860 tonnes and 2,835 tonnes: these new entrants exported a total of 9,116 tonnes.

Ventura dominates in Europe, while Sekoya Pop is relevant in the United Kingdom and other markets

The varietal data highlights differentiated strategies by destination. In Europe, the dominant variety is Ventura, with a 44% share, followed by Sekoya Pop with 15%, Biloxi with 10% and Emerald with 7%. In the United States, Ventura is also the leading variety, although with a more limited share of 18%, followed by Biloxi, Sekoya Pop, Magica and Rocio.

In the United Kingdom, the breakdown appears more focused on premium and recognizable varieties: Ventura accounts for 29%, Sekoya Pop for 25%, Rocio for 12% and Magica for 11%. In other markets, by contrast, the leading variety is Sekoya Pop with 22%, ahead of Magica, Ventura, Emerald and Biloxi.

A positive final balance, but with new commercial challenges

The overall balance of the 2025-26 season is positive: Peru is growing significantly again, consolidating its international leadership and strengthening its presence in key markets. However, volume growth also reopens the issue of balance between supply, prices and perceived quality.

For European markets, the most relevant figure is the 34% increase in shipments to Europe. This strengthens Peru’s role as an essential supplier in the counter-season window, but also increases competitive pressure on origin, programming, quality standards and varietal differentiation. In a category where the end consumer is increasingly sensitive to the eating experience, the challenge will not only be to export more blueberries, but to maintain consistency in taste, firmness, size and shelf life.

The Proarándanos final report therefore confirms a clear trend: Peruvian blueberries are growing again, but the new phase of global competition will not be based on volumes alone. The ability to segment supply, enhance varieties, serve premium markets and guarantee quality continuity will be decisive in transforming production growth into stable value for the entire supply chain.