In 2025, the currant market in Italy shows signs of recovery compared with 2024, but still within a fragile five-year framework. Over the last year, the number of buyers has increased sharply, penetration has risen, total volumes have recovered, and overall value has returned to growth as well.

At the same time, however, almost all indicators of purchase intensity continue to worsen: volume per buyer declines, volume per occasion decreases, frequency falls, and both spending per buyer and spending per occasion contract.

The overall reading is therefore that of a category which, in 2025, grows mainly through an expanded buyer base and a partial recovery in overall volumes, but still does not show consolidation in terms of depth of consumption.

For the supply chain, the signal is twofold: currants are managing to return to more households, but they remain a category characterised by light purchasing dynamics and structural discontinuities over the medium term.

Basic indicators and market reach

The reference base, namely Italian households, rises from 26.114 million in 2024 to 26.563 million in 2025, an increase of 449 thousand households, equal to +2.7%. For this KPI, 2021 data are not available in the table, while the observable period from 2022 to 2025 shows gradual and steady growth.

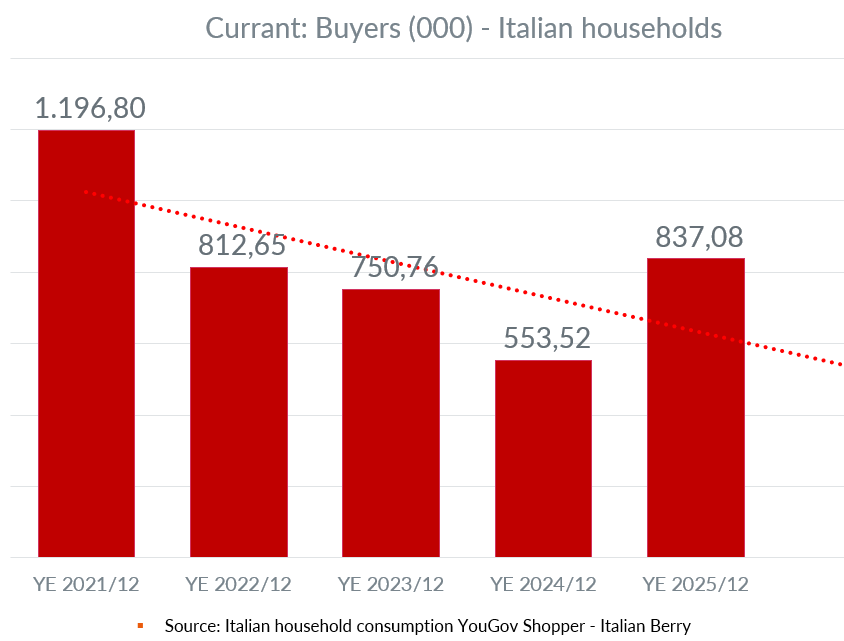

Currant buyers increased from 554 thousand in 2024 to 837 thousand in 2025, with an increase of 284 thousand households and a change of +51.2%. This is one of the strongest signals in the entire table.

However, the five-year trend remains highly uneven: from 1.197 million in 2021 it fell to 813 thousand in 2022, then to 751 thousand in 2023 and 554 thousand in 2024, before the recovery in 2025. This is therefore a clear rebound after a decline, but the latest year still remains well below the 2021 level.

Penetration also improved significantly. In 2025 it reached 3.15%, compared with 2.12% in 2024, an increase of 1.03 points and +48.7%. Over the five-year period, however, the underlying picture remains negative: from 4.59% in 2021 it fell to 3.18% in 2022, then to 2.93% in 2023 and 2.12% in 2024, before recovering in 2025.

Here too, we are looking at a rebound after a long contraction, still insufficient to bring currants back to the initial levels of the series.

These three KPIs indicate that in 2025 the currant market returned to growth above all through broader reach. The product managed to win back part of the buyer base lost in previous years, but it remains a niche category, with still limited penetration in the basket of Italian households.

Volumes: recovery in 2025, but increasingly weaker intensity

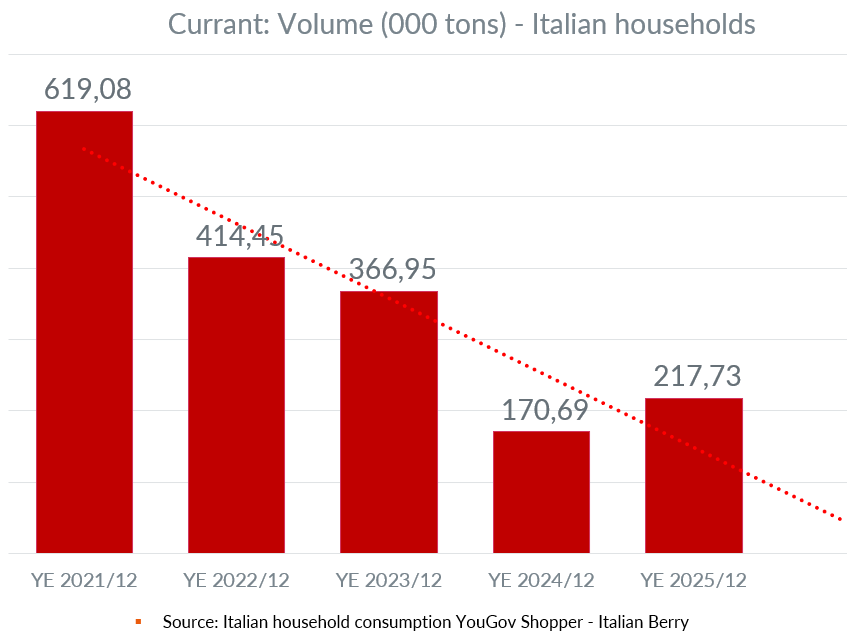

Total volume stood at 218 tonnes in 2025, up from 171 tonnes in 2024. The change was 47 tonnes, equal to +27.6%. Over the five-year period, however, the path remains very irregular and overall downward: 619 tonnes in 2021, 414 in 2022, 367 in 2023, 171 in 2024 and finally 218 in 2025.

The latest-year figure signals a recovery after a sharp decline, but the level remains far below that of the first years of the series.

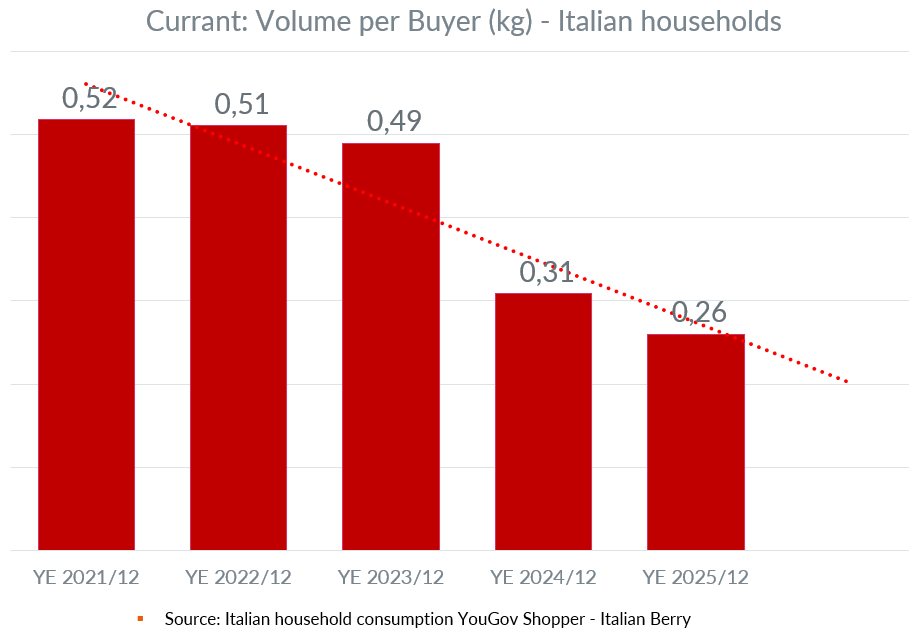

Volume per buyer, on the other hand, continued to deteriorate. In 2025 it fell to 0.26 kg, compared with 0.31 kg in 2024, a reduction of 0.05 kg and -15.7%. The five-year trend clearly points to structural decline: 0.52 kg in 2021, 0.51 kg in 2022, 0.49 kg in 2023, 0.31 kg in 2024 and 0.26 kg in 2025. It is one of the most critical KPIs in the table, because it indicates that each buyer is purchasing increasingly smaller quantities.

Volume per occasion also continued its downward path. In 2025 it stood at 0.16 kg, compared with 0.18 kg in 2024, a change of -0.02 kg and -11.7%. Here too, the five-year period shows a trajectory of structural decline: 0.33 kg in 2021, 0.32 kg in 2022, 0.26 kg in 2023, 0.18 kg in 2024 and 0.16 kg in 2025. The figure suggests a progressive lightening of purchase acts.

Purchase frequency fell from 1.76 occasions in 2024 to 1.68 in 2025, a reduction of 0.08 occasions and -4.5%. Over the five-year period, behaviour was more uneven: 1.57 in 2021, 1.57 in 2022, rising to 1.87 in 2023, then easing to 1.76 in 2024 and 1.68 in 2025. In this case there is no linear collapse, but rather relative stability at low levels, with weakening over the last two years.

The combined reading of the volume KPIs is very clear. In 2025, currants were bought by more households, but consumers purchased them less frequently and above all in smaller quantities, both per buyer and per single occasion.

The recovery in total volumes therefore stemmed from the expansion of the buyer base, not from greater purchase intensity. This remains the category’s main structural weakness.

Value and spending: the market grows, but on still fragile foundations

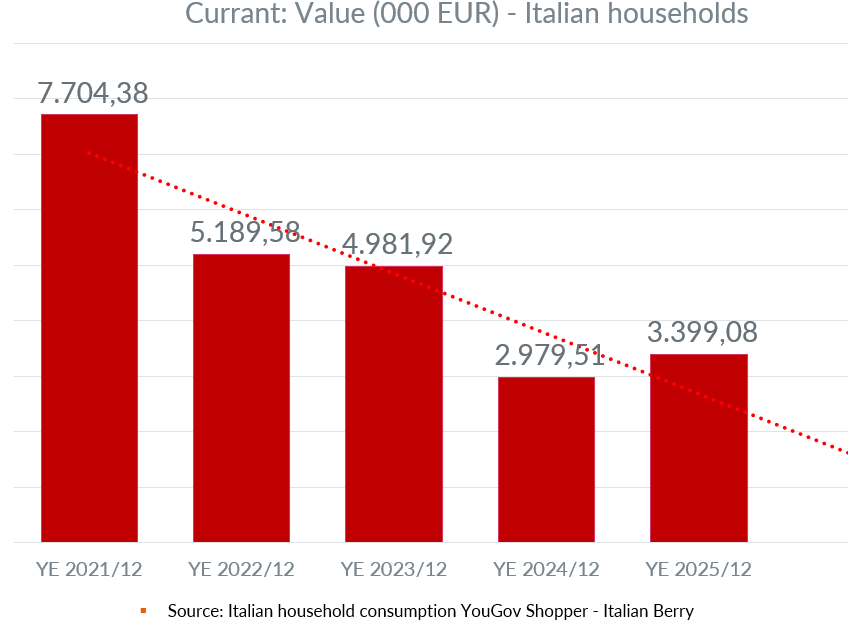

The overall value of the currant market reached €3.399 million in 2025, up from €2.980 million in 2024. Growth amounted to €420 thousand, equal to +14.1%.

Looking at the five-year period, however, the profile remains weak: €7.704 million in 2021, €5.190 million in 2022, €4.982 million in 2023, €2.980 million in 2024 and €3.399 million in 2025. We are therefore facing a recovery in the latest year, but within a still negative medium-term trajectory.

Spending per buyer declined sharply, falling from €5.38 in 2024 to €4.06 in 2025, a change of -€1.32 and -24.6%. Over the five-year period, the decline is very marked: €6.44 in 2021, €6.39 in 2022, €6.64 in 2023, €5.38 in 2024 and €4.06 in 2025. This is another KPI signalling structural decline and a progressive loss of value generated by each buyer.

Spending per occasion also fell from €3.07 in 2024 to €2.42 in 2025, a contraction of €0.64 and -21.0%. The five-year trend is also downward: €4.11 in 2021, €4.06 in 2022, €3.56 in 2023, €3.07 in 2024 and €2.42 in 2025. The dynamic reflects increasingly smaller purchases and a downsizing of the economic value per purchase act.

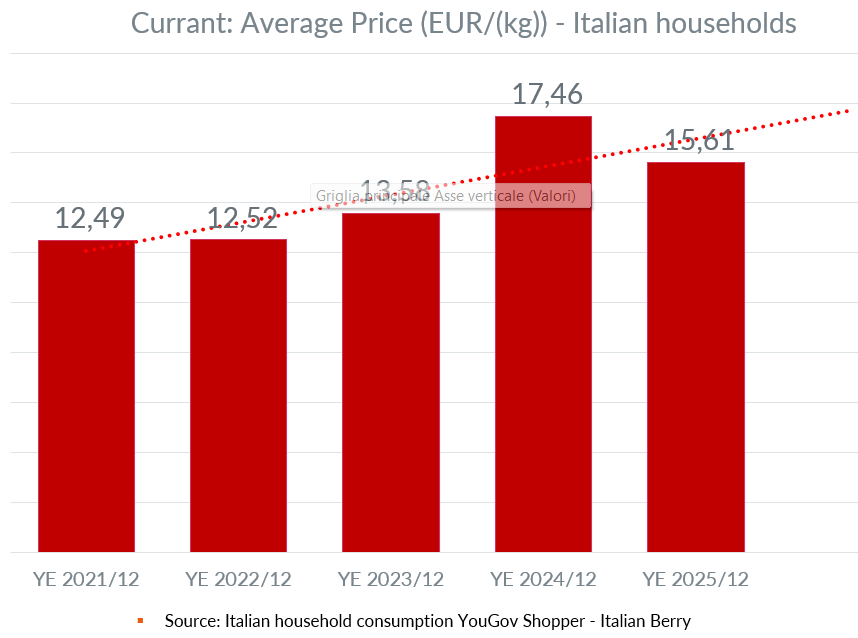

Average price, unlike what has been observed in other berry categories, declined in 2025: it fell from €17.46/kg in 2024 to €15.61/kg in 2025, a change of -€1.84/kg and -10.6%. Over the five-year period, the pattern is uneven: €12.49/kg in 2021, €12.52 in 2022, €13.58 in 2023, a sharp increase to €17.46 in 2024, and then a correction to €15.61 in 2025. It remains above 2021-2023 levels, but the most recent comparison shows a clear correction.

The economic reading is therefore different from other categories. In 2025, the value of the currant market grew mainly because of the recovery in total volumes and the increase in buyers, not because of price, which actually moved lower.

The most positive figure is the category’s return to more shopping baskets; the most problematic one is that each buyer is generating ever lower average spending.

Loyalty: slight weakening after the 2023 peak

The repeat rate stood at 32.32% in 2025, slightly down from 33.54% in 2024. The change was -1.23 points, equal to -1.2%. The 2021 figure is not available in the table. The observable series shows a fluctuating trend: 30.68% in 2022, rising to 39.77% in 2023, then falling to 33.54% in 2024 and 32.32% in 2025.

The signal remains weak. Currants are managing to recover buyers, but they still struggle to consolidate real continuity in repeat purchasing. On the loyalty front too, 2025 still does not show structural strengthening of the category.

2025 marks a rebound, but the market still needs consolidation

Over the 2021-2025 period, the Italian currant market shows a long downsizing phase, interrupted in 2025 by a significant recovery in buyers, penetration, volumes and overall value. This is the main positive element of the latest year: the category once again reached a broader share of Italian households and brought purchasing traffic back.

At the same time, the comparison between 2024 and 2025 highlights a very clear strategic issue. Recent growth has been driven almost exclusively by the expansion of the buyer base, while the KPIs measuring depth of consumption have worsened: volume per buyer, volume per occasion, frequency, spending per buyer, spending per occasion and repeat rate.

Average price also fell, signalling a less supportive environment in terms of unit value.

The phase experienced by currants in 2025 can therefore be defined as an extensive rebound, positive but still not consolidated.

For the supply chain, the challenge is not only to continue recruiting new buyers, but above all to strengthen purchase intensity, increase average quantity per act, improve frequency and build greater loyalty. It is on these KPIs that the currant category’s ability to turn the 2025 recovery into more stable and structured growth will be measured.