2025 data confirm a very clear trend: blueberry consumption in Italy is progressively becoming less “niche” and less concentrated in a few segments, with a broader purchasing base across areas and social groups that in the past were farther from the national average.

The overall picture shows two parallel phenomena:

- reduction of some historical gaps (especially geographic and socio-economic);

- persistence of qualitative differences in purchasing behavior, especially by age of the main shopper and household structure.

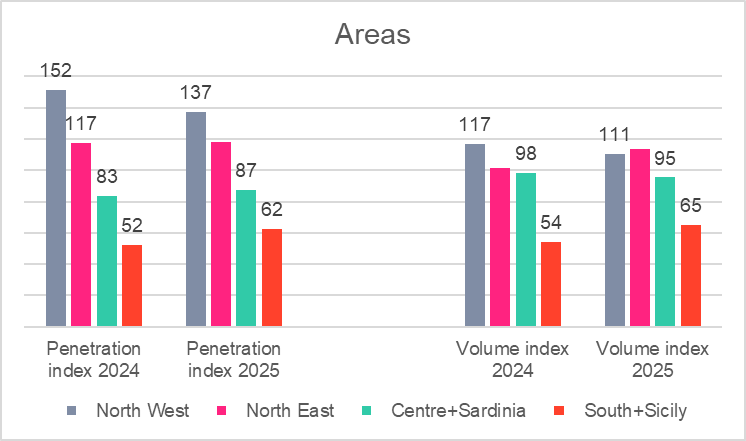

Geography: the North-South gap is narrowing, but the North remains ahead

Geography continues to influence blueberry consumption, but to a lesser extent than in the past.

Penetration: blueberries are becoming a national product

In 2025, the North-West remains the area with the highest penetration (index 137, Italy=100), but the figure is down compared with 2024 (152). By contrast:

- Centre+Sardinia rises from 83 to 87

- South+Sicily rises from 52 to 62

This means blueberries are still more present in shopping baskets in the North, but the gap with the rest of the country is shrinking. In other words, penetration is progressively becoming more uniform.

The North-East is the only macro-area already close to the national average that shows further strengthening, moving from 117 to 118, a sign of a mature but still dynamic market.

Volumes: strong recovery in the South, acceleration in the North-East

Convergence is also emerging in quantities purchased:

- South+Sicily: from 54 to 65

- Centre+Sardinia: from 98 to 95 (broadly stable, with a slight decline)

- North-West: from 117 to 111 (down, but still above average)

- North-East: from 101 to 114 (strong growth)

The most interesting figure is the South: the volume index rises from 54 to 65, so it is no longer “just over half” of the average, but is approaching two-thirds of the national average. This is an important improvement, indicating a phase of category expansion even in historically weaker areas.

From a geographic perspective, blueberries remain more established in the North, but in 2025 a process of territorial normalization is clearly visible. The product is spreading more widely and is less dependent on area of residence.

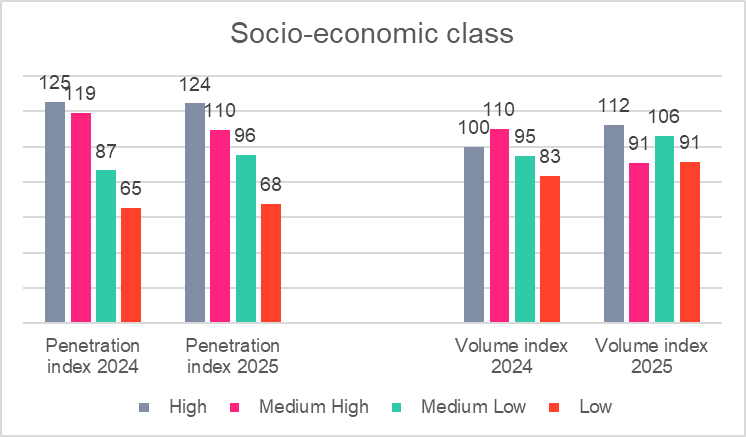

Socio-economic class: penetration remains selective, but volumes are rebalancing

The link between blueberry consumption and socio-economic class remains clear, especially for penetration (how many households buy at least once), but in 2025 an interesting shift can be seen in volumes.

Penetration: the gap remains, but narrows in the middle-lower segments

2025 penetration by socio-economic class is:

- High: 124

- Medium High: 110

- Medium Low: 96

- Low: 68

The data confirm that blueberries are still more widespread among households with greater spending capacity, but there is a recovery in the weaker segments:

- Medium Low rises from 87 to 96

- Low rises from 65 to 68

At the same time, the Medium High segment falls from 119 to 110, while the High segment remains broadly stable (125 → 124).

This suggests blueberries are gradually moving beyond the “more premium” consumption perimeter and are becoming more accessible also to intermediate and middle-lower segments.

Volumes: strong redistribution across classes

The most marked change is in purchased volumes:

- High: from 100 to 112

- Medium High: from 110 to 91 (sharp decline)

- Medium Low: from 95 to 106 (strong growth)

- Low: from 83 to 91 (growth)

In 2025, volumes are therefore less polarized than in the previous year and are shifting partly toward middle-lower classes. This is a very important signal, because it indicates that category growth no longer depends only on the most affluent households.

From a socio-economic point of view, penetration therefore remains correlated with income/social positioning, but purchase intensity (volume) shows greater democratization, with a recovery in lower-income and middle-lower segments.

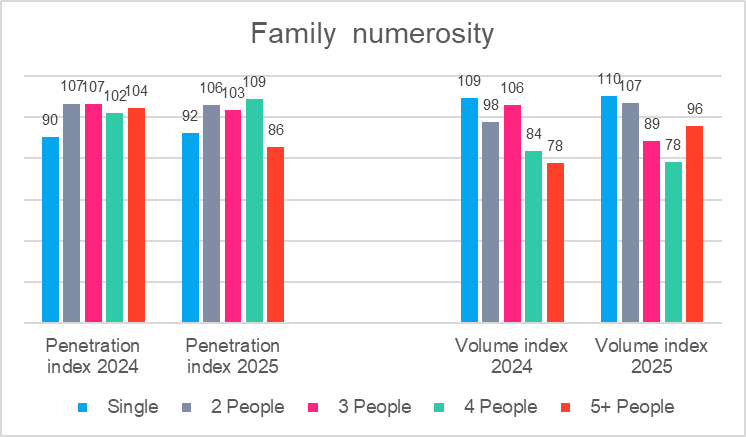

Household size: a more complex picture, with mixed signals

Household size has a significant effect on consumption, but 2025 data show a less linear pattern than it may seem.

Penetration: sharp decline in 5+ households, growth in 4-person households

2025 penetration indexes:

- Single: 92

- 2 people: 106

- 3 people: 103

- 4 people: 109

- 5+ people: 86

The clearest signal is the decline in large households (5+ members), which fall from 104 to 86 in penetration: therefore, in 2025 it is less common to find blueberry buyers among very large households than in 2024.

By contrast, 4-person households increase (from 102 to 109), becoming the group with the highest penetration.

Volumes: growth in 5+ households, but decline in 3- and 4-person households

On quantities purchased, 2025 data are:

- Single: 110

- 2 people: 107

- 3 people: 89

- 4 people: 78

- 5+ people: 96

An interesting dynamic emerges here:

- 5+ households increase volume from 78 to 96 (very strong recovery)

- 3-person households fall from 106 to 89

- 4-person households fall from 84 to 78

So your point is correct regarding the recovery of large households in volume terms, but it should be clarified that this recovery occurs despite a decline in penetration: in practice, in 2025 there are fewer 5+ households buying blueberries, but those that do buy purchase much more than in 2024.

As for household size, there is no simple linear relationship between number of members and consumption. 2025 data instead suggest a segmentation of behaviors:

- small households (singles and couples) with volumes consistently above average;

- 3–4 person households slowing down;

- 5+ households less widespread as buyers, but with greater purchase intensity.

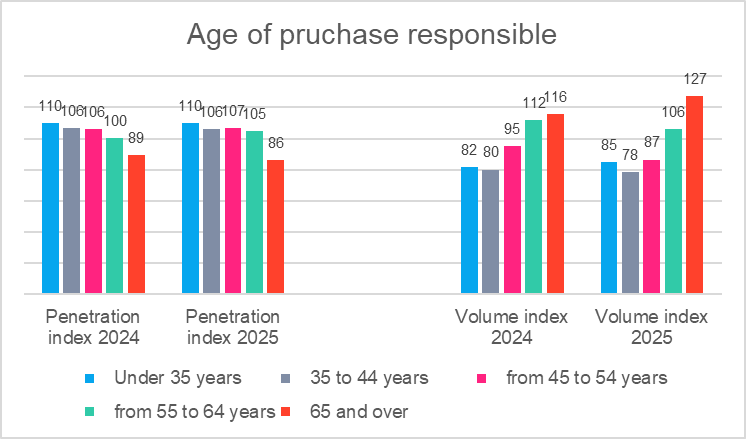

Age of the main shopper: lower penetration with age, but higher volumes among older consumers

This is one of the strongest and clearest patterns in the whole analysis.

Penetration: higher among younger consumers, lower among older consumers

2025 penetration indexes:

- Under 35: 110

- 35–44 years: 106

- 45–54 years: 107

- 55–64 years: 105

- 65+: 86

Penetration therefore remains higher in age groups up to 54, while it drops sharply among over-65s. This indicates that blueberries are still more “familiar” and more present in the purchasing habits of households with a younger or middle-aged main shopper.

Volumes: over-65s buy less often, but buy more

2025 volume indexes:

- Under 35: 85

- 35–44 years: 78

- 45–54 years: 87

- 55–64 years: 106

- 65+: 127

Here the relationship reverses completely. Households with an older main shopper are less numerous among buyers, but when they buy blueberries, they purchase quantities above the average.

The clearest case is the 65+ segment, with a volume index of 127, up sharply from 116 in 2024. It is the highest value among all age segments analyzed.

Blueberries therefore seem to have a “double-track” profile:

- among younger consumers they are a more widespread product, but with lighter average purchases;

- among older consumers they are bought by a narrower group, but with greater intensity.

This may reflect several factors (eating habits, consumption frequency, health motivations, household shopping organization).

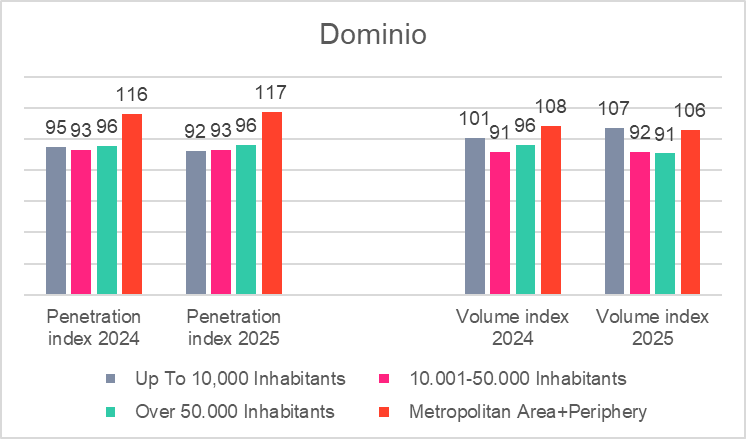

Urban domain: moderate effect, with a stable advantage for metropolitan areas

The territorial variable linked to urban size confirms an impact that is present but less marked than other variables (geographic area, age, socio-economic class).

Penetration: metropolitan areas above average

2025 penetration indexes:

- Up to 10,000 inhabitants: 92

- 10,001–50,000 inhabitants: 93

- Over 50,000 inhabitants: 96

- Metropolitan area + periphery: 117

Metropolitan areas remain the main driver of category diffusion: penetration is 17% above the national average, slightly up compared with 2024 (116 → 117).

Volumes: limited differences, but cities are not always the leaders

2025 volume indexes:

- Up to 10,000 inhabitants: 107

- 10,001–50,000 inhabitants: 92

- Over 50,000 inhabitants: 91

- Metropolitan area + periphery: 106

Interestingly, while penetration is higher in metropolitan areas, volumes are not exclusive to large cities: even small towns (up to 10,000 inhabitants) in 2025 show a volume index of 107, above average and increasing (from 101).

Urban domain summary: the metropolitan city remains the context where it is easiest to find buying households, but purchased volumes are now spread more widely and show good vitality even in smaller towns.

Possible cross-cutting interpretations

1. Blueberries are increasingly less a “wealthy Northern” product

Compared with the past, consumption is broadening:

- geographically (recovery in the South and Centre),

- socially (growth in medium-low and low segments),

- territorially (good signs also outside metropolitan areas).

2. Penetration and volume tell two different stories

Many segments show opposite behaviors between:

- penetration = how many households buy

- volume = how much they buy

This is particularly evident for:

- over-65s (fewer buyers, but stronger buyers),

- 5+ households (less widespread but recovering in volumes),

- middle-lower socio-economic classes (more present and more active).

3. 2025 looks like the year of “normalization”

The most strategic point is that blueberries are moving out of a growth phase driven by a few “leading” clusters and entering a more mature phase, with a broader and more homogeneous consumer base.

Conclusions

In 2025, blueberries therefore confirm a dual evolution: on the one hand, they remain a category with distinctive traits (strong presence in the North, higher penetration in upper socio-economic classes, high purchase intensity among over-65s); on the other hand, they show increasingly clear signs of structural market broadening.

It is precisely this combination—growth and normalization—that makes blueberries one of the most interesting categories to watch in Italy’s fresh fruit market.